We spend a lot of time talking about how to get into crypto, on-ramps, DCA strategies, yield, airdrops. But at some point, we all hit the same very real question:

“How do we actually off ramp crypto and get this money into our bank account… without getting wrecked by fees, scams, or tax confusion?”

That’s where crypto off-ramping comes in. It’s the bridge from our on-chain wealth to rent, groceries, mortgages, or that vacation we keep promising ourselves.

In this guide, we’ll break down what off-ramping really means, the main ways to off ramp crypto, how to choose the right method for your situation, and the security and tax issues we can’t ignore. We’ll keep it clear, practical, and grounded in how people actually move money today.

What Crypto Off-Ramping Actually Means (And Why It Matters)

When we off ramp crypto, we’re converting digital assets like BTC, ETH, USDC, or altcoins back into traditional money, usually USD, EUR, or another local fiat currency, and sending it to a bank account, card, or payment app.

If on-ramping is how we go from dollars to crypto, off-ramping is that process in reverse.

Why it matters:

- Liquidity – We can actually use our gains in the real world, not just watch numbers go up (or down) on a screen.

- Risk management – In a volatile market, off-ramping lets us lock in profits, de-risk, or build cash reserves.

- Trust in the system – If we can’t get money out easily and safely, the whole crypto ecosystem feels like a closed casino, not a serious financial stack.

Most major exchanges and platforms now support some form of off-ramp, but they’re not all equal. Some are fast but expensive, others are cheap but slow, and some add extra risk we don’t want.

The goal of this article is to help us treat off-ramping like a strategy, not a last-minute panic move when markets pump or dump.

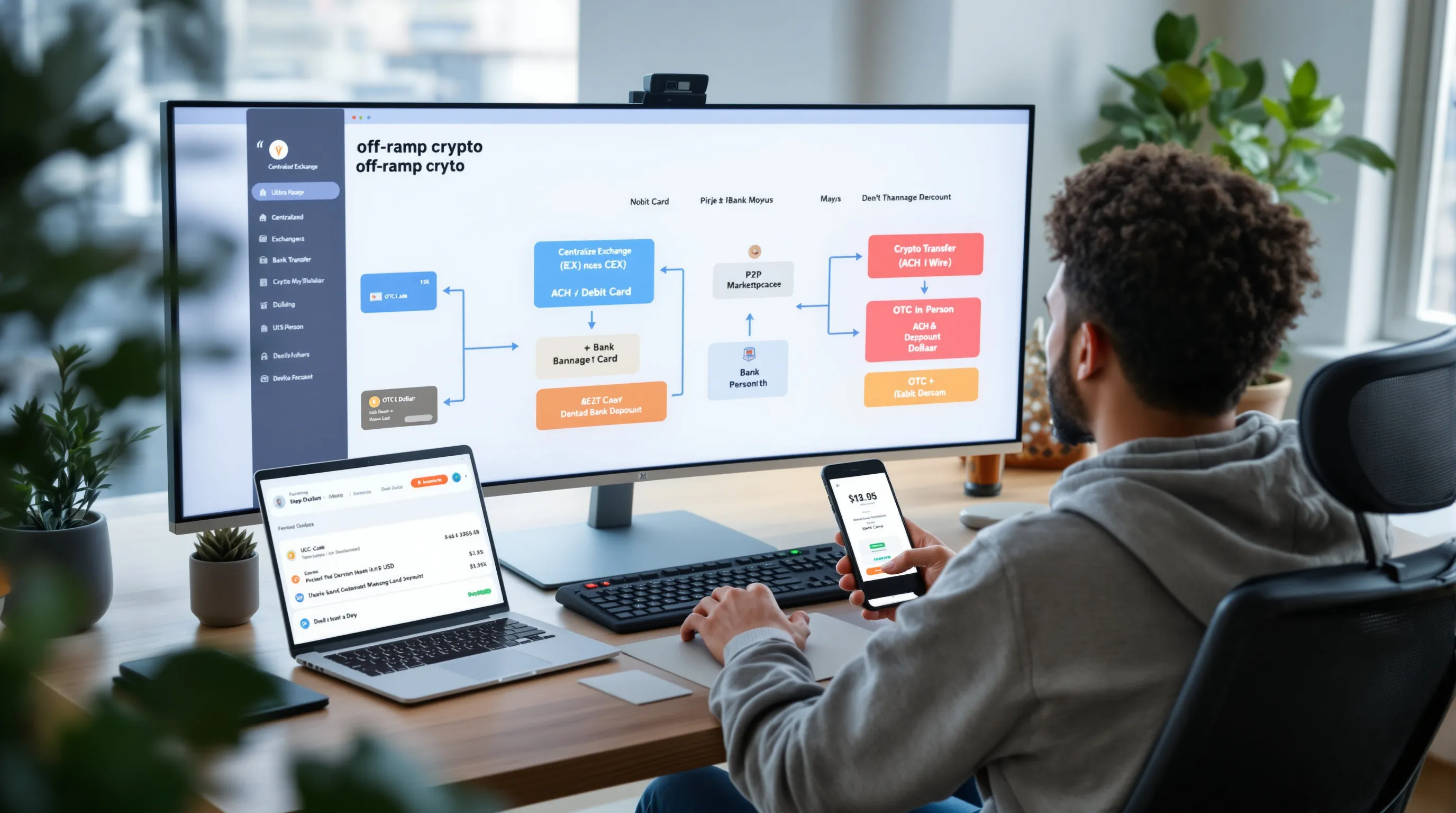

Main Ways To Off-Ramp Crypto Into Fiat

There’s no single “best” way to off ramp crypto. The right choice depends on our size, urgency, and risk tolerance. Here are the main options and where they shine.

Centralized Exchanges (CEXs)

Centralized exchanges like Coinbase, Kraken, Binance (in allowed regions), and others are still the most common off-ramps.

Basic flow:

- Send crypto from our wallet to the exchange.

- Sell it for fiat (USD, EUR, etc.).

- Withdraw to a bank using ACH, wire, or SEPA.

Pros

- Easy UX, ideal for beginners.

- Deep liquidity for majors like BTC, ETH, and top altcoins.

- Clear reporting and exportable history.

Cons

- KYC required, so less privacy.

- Funds are custodial while on the exchange.

- Occasional delays or limits on withdrawals.

Peer-To-Peer (P2P) Marketplaces

P2P platforms let us sell crypto directly to another person for fiat through bank transfer, cash, or local rails. Think of it as a crypto version of Craigslist, but with an escrow middle layer.

Pros

- Can support local payment methods that big exchanges don’t.

- Sometimes better rates in niche markets.

- More decentralized, especially on platforms that don’t hold funds.

Cons

- Higher risk of fraud or chargebacks.

- Requires careful vetting of buyers/sellers.

- Takes more time and effort than a CEX.

If we go this route, we should only use platforms with escrow, reputation scores, and strong dispute handling.

Crypto Debit Cards And Payment Apps

A lot of platforms now offer crypto debit cards or app-based off-ramps (for example, products from exchanges and fintechs that auto-convert crypto when we spend).

How it works:

- We load crypto into the app.

- When we tap the card or pay online, the app sells just enough crypto to cover the purchase.

Pros

- Super convenient for everyday spending.

- No manual off-ramp steps once it’s set up.

Cons

- Fees can be baked into spreads.

- Not ideal for very large amounts.

- Regulatory and KYC rules still apply.

Bank Transfers, Wires, And ACH Off-Ramps

Most CEXs and some broker-style apps let us off ramp crypto straight to:

- ACH transfers (US) – cheap but can take 1–3 business days.

- Wires – faster for large amounts, higher bank fees.

- SEPA (EU) – common and fairly quick.

We usually sell the crypto on-platform first, then withdraw the fiat. This is often the cleanest paper trail for taxes.

In-Person And OTC Off-Ramping

For higher net-worth moves, we see more use of:

- OTC desks that handle large block trades off order books.

- In-person deals (with serious security practices).

Pros

- Better pricing and less slippage for large tickets.

- More privacy and white-glove support with legit OTC desks.

Cons

- Not necessary for smaller amounts.

- Must avoid sketchy in-person cash deals, huge scam and safety risk.

For amounts that would hurt badly if lost, we want regulated OTC desks with clear contracts, not back-alley trades.

How To Choose The Right Off-Ramp For Your Situation

Before we rush to off ramp crypto, we should match the method to our needs: size, speed, regulation comfort, and privacy.

Jurisdiction, KYC, And Regulatory Comfort Level

Where we live matters. US users, EU residents, and people in more restricted countries all face different rules.

Ask ourselves:

- Is this off-ramp licensed in my country or state?

- Am I comfortable with full KYC (ID, address, source of funds)?

If we want lower friction with regulators and banks, CEXs that operate under local rules are usually safer than sketchy offshore options.

Liquidity, Speed, And Supported Assets

Not every coin is easy to off-ramp.

- Large caps (BTC, ETH, major stablecoins) are liquid almost everywhere.

- Tiny altcoins may need a swap to USDT/USDC/ETH first.

We should check:

- Daily withdrawal limits

- Estimated processing times

- Which chains and tokens are supported

For urgent exits (e.g., we need funds tomorrow), we might prefer a CEX with ACH + instant-sell options.

Counterparty Risk And Custody Considerations

Whenever we hand over custody of our assets, we’re taking counterparty risk, the risk that the exchange, app, or desk fails, freezes, or abuses funds.

To reduce it:

- Only keep funds on custodial platforms for as long as needed.

- Prefer well-known, regulated players with a solid track record.

- Avoid leaving large amounts sitting on small or opaque services.

Privacy Trade-Offs And Data Sharing

More convenience usually means less privacy.

- CEXs and banks report more data to regulators.

- P2P and crypto-native off-ramps can be more private but come with higher operational risks.

We need to balance:

- Our legal obligations in our country.

- Our personal comfort with data sharing.

- The real-world need (paying a mortgage vs. experimenting with small amounts).

Step-By-Step: Off-Ramping Crypto Safely

Let’s walk through a clean off-ramp flow that works for most people, using a centralized exchange plus bank withdrawal as an example.

Prepare Your Wallets And Verify Your Identity

- Make sure our funds are in a wallet we control and can send from.

- Pick a reputable off-ramp (exchange or app) that supports our country and assets.

- Complete KYC and enable 2FA (authenticator app > SMS).

Do this before we need the money urgently. Verification can sometimes take a day or more.

Move Funds From Self-Custody To Your Off-Ramp

Next:

- Copy the deposit address from our off-ramp platform.

- Double-check chain and address (send a tiny test amount first).

- Send the full amount once we’re sure everything matches.

We should wait for enough confirmations on-chain before trading, especially on slower networks like Bitcoin.

Execute The Sale And Select Your Payout Method

Once the crypto is on the platform:

- Place a market or limit sell order into fiat or a stablecoin.

- For larger amounts, consider using limit orders to reduce slippage.

- Choose the payout route: ACH, wire, SEPA, or card withdrawal.

We also want to note any minimum withdrawal amounts or bank acceptance guidelines.

Confirm Settlement And Secure Your Remaining Crypto

After we hit withdraw:

- Track status in the exchange app (pending, processing, completed).

- Watch for email or SMS confirmations.

- Confirm final arrival in the bank or payment app.

Any crypto we’re not off-ramping should go back to secure storage, hardware wallet or multisig, not linger on the exchange.

Track Your Transactions For Reporting

Every off-ramp event is a taxable disposition in many countries, including the US.

We should:

- Export CSVs from exchanges and wallets.

- Tag transfers, swaps, and sales in a portfolio tracker or tax tool.

- Save screenshots or PDFs of big withdrawals in case our bank or accountant asks later.

Fees, Taxes, And Compliance You Can’t Ignore

Fees and taxes can quietly eat into our gains if we’re not paying attention.

Trading Fees, Spreads, And Slippage

When we off ramp crypto, costs show up in several places:

- Trading fees – Usually 0.1%–1% depending on the platform and our volume.

- Spread – The difference between buy and sell price: often wider for illiquid tokens.

- Slippage – Price impact when our order size moves the market.

We can reduce this by:

- Off-ramping in liquid pairs (BTC, ETH, USDC/USDT).

- Using limit orders instead of large market dumps.

Deposit, Withdrawal, And Network Fees

We also pay:

- Network gas fees to move crypto into the off-ramp.

- Withdrawal fees for ACH, wire, or card payouts.

Many US exchanges offer free ACH but charge for instant withdrawals or wires. It’s worth checking fee pages before moving large amounts.

Capital Gains, Holding Periods, And Tax Lots

In countries like the US, each sale of crypto is usually a capital gains event.

Key concepts:

- Short-term vs. long-term – Hold > 1 year and we may pay a lower long-term rate.

- Tax lots – Specific units of an asset with their own cost basis.

Off-ramping from a bag we bought last week vs. three years ago can have very different tax outcomes.

Tools And Habits For Clean Crypto Accounting

We can make our future selves (and our CPA) a lot happier by:

- Using tools like Koinly, CoinTracker, or CoinTracking to sync wallets and exchanges.

- Keeping personal notes for unusual events (airdrops, refunds, OTC deals).

- Reviewing our year-to-date gains before big off-ramps, not after.

This isn’t about perfection. It’s about having a defensible, consistent record if the tax office ever comes knocking.

Security Risks And How To Avoid Common Off-Ramp Traps

Off-ramping touches three risky worlds at once: crypto, banks, and the open internet. A bit of paranoia is healthy.

Phishing, Fake Off-Ramps, And Social Engineering

Scammers love the phrase “off ramp crypto“ because they know people are moving real money.

Red flags:

- Domains that look almost like a major exchange.

- DMs offering “better rates” for your off-ramp.

- Fake customer support accounts asking for seed phrases.

We should:

- Type URLs manually or use password manager bookmarks.

- Never share seed phrases or private keys with anyone.

- Verify support channels via official websites.

Account Takeovers And SIM Swaps

Once an attacker controls our email, phone, or SIM card, they can often reset exchange logins.

Mitigation:

- Use app-based 2FA (Google Authenticator, Authy, hardware keys).

- Avoid SMS as the only 2FA factor.

- Lock down phone accounts with extra PINs where carriers allow it.

Jurisdictional Restrictions And Frozen Accounts

Sometimes accounts get frozen not because of hacking, but due to compliance checks or unclear regulations.

We can lower the odds by:

- Avoiding large sudden transfers from high-risk jurisdictions.

- Keeping documentation of where funds came from (exchanges, salary, mining, etc.).

- Staying inside a platform’s published limits and guidelines.

Operational Best Practices For Ongoing Safety

Over time, small habits compound into strong protection:

- Separate “hot” spending wallets from long-term cold storage.

- Use different emails for banking and crypto if possible.

- Regularly review which devices and apps have access to our accounts.

The goal isn’t zero risk, that’s impossible. It’s to make ourselves a hard target so attackers move on to someone else.

The Future Of Crypto Off-Ramps: Stablecoins, On-Chain Credit, And Beyond

Off-ramping is already changing fast. We’re moving from “sell to bank“ to a more blended world of on-chain and off-chain money.

Crypto-Native Off-Ramps: Stablecoins, On-Chain FX, And RWAs

We’re seeing more people treat regulated stablecoins (USDC, fully-backed USDT alternatives, etc.) as a kind of halfway house between pure crypto and bank cash.

Instead of fully off-ramping, we might:

- Move into stablecoins during volatility.

- Use on-chain foreign exchange (FX) to switch between digital dollars and euros.

- Tap real-world asset (RWA) protocols for tokenized treasuries or bonds.

This keeps value in the crypto stack while reducing volatility.

Non-Custodial, Composable Off-Ramps In DeFi

DeFi is also building non-custodial off-ramps:

- Protocols that plug into bank APIs or fintech rails.

- Aggregators that route funds through the cheapest or fastest off-ramp.

In time, we may be able to:

Sign a single on-chain transaction, and funds automatically flow through DEXs, bridges, and off-ramps into our bank with minimized fees and slippage.

All while retaining self-custody until the very last hop.

AI Agents, Automation, And Intent-Based Off-Ramping

AI is creeping into this too.

We can imagine:

- AI agents that monitor our portfolio and suggest off-ramp timing based on volatility or personal rules.

- “Intent-based“ systems where we say, “I want $5,000 in my bank by tomorrow with max 0.5% fees“, and the stack figures out the best route.

The infrastructure isn’t perfect yet, but the direction is clear: smarter, safer, and more automated off-ramps that still leave us in control.

Conclusion

Off-ramping is where theory meets reality. It’s the moment our beliefs about crypto turn into rent, tuition, or freedom to walk away from a job we don’t love.

If we treat off-ramping as an afterthought, we end up with:

- Surprise fees

- Tax headaches

- Frozen accounts

- Or worst-case, funds lost to scams

If we treat it as a core part of our crypto strategy, we get:

- Clear options for how and when to exit

- Better tax positioning

- Higher security and less stress

As we keep building in this space, it’s worth asking ourselves:

“If I needed to off ramp crypto in size next month, quickly, safely, and legally, what’s my plan?”

If we can answer that with confidence, we’re already ahead of most of the market.

Disclaimer: This content is for informational purposes only and does not constitute financial or investment advice.